Murphy USA (MUSA)·Q4 2025 Earnings Summary

Murphy USA Beats Q4 EPS as Fuel Margins Surge, Stock Rises 2%

February 04, 2026 · by Fintool AI Agent

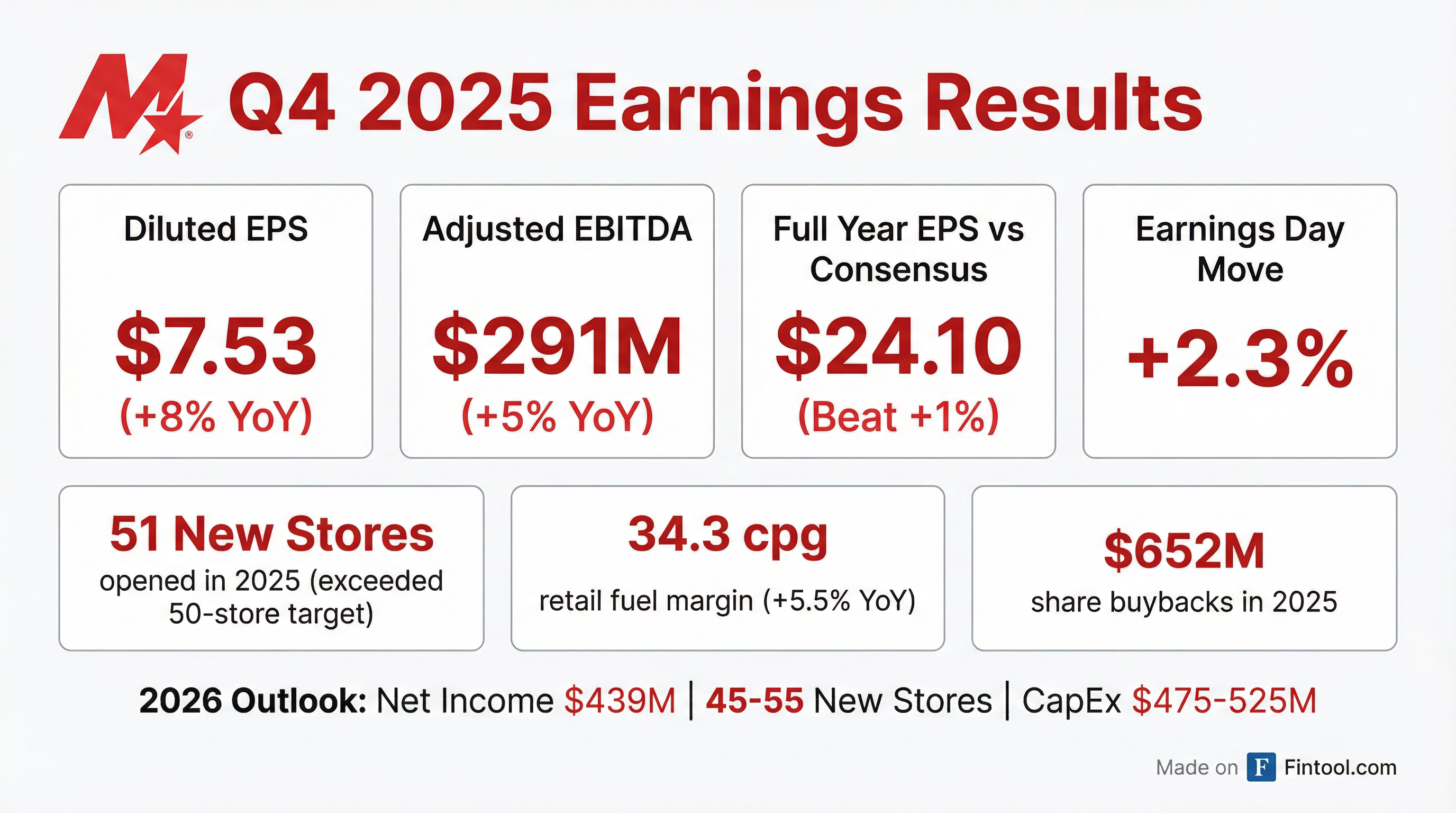

Murphy USA delivered a solid Q4 2025, beating EPS estimates by approximately 6% as retail fuel margins expanded to 34.3 cpg, the highest level in eight quarters . The convenience store and fuel retailer posted diluted EPS of $7.53 compared to $6.96 in Q4 2024, a +8.2% year-over-year improvement . The stock responded positively, rising 2.3% to close at $444.85 on earnings day.

Did Murphy USA Beat Earnings?

Yes — Murphy USA beat on EPS while revenue came in roughly in-line with expectations.

Full-Year 2025 Results:

*Values retrieved from S&P Global

The Q4 EPS beat was driven by strong fuel contribution despite net income remaining flat year-over-year. Share buybacks continued to provide EPS tailwinds, with diluted shares outstanding declining 8% to 18.8 million from 20.5 million .

What Drove the Quarter?

Fuel Contribution Surged

The standout metric was retail fuel margin of 34.3 cpg, up from 28.9 cpg in Q4 2024 — a 15.6% improvement . Total fuel contribution dollars increased 8.9% to $423.6 million .

CEO Mindy West attributed the margin expansion to favorable market volatility: "Fourth quarter retail margins were 2 cents higher than the prior year, responding favorably as higher levels of volatility were introduced to the market" .

On the call, West clarified the investment needed to maintain share: "We will still need to protect our position, especially against competitive entrants in certain markets, by putting 1-2 cents on the street" . She also noted the structural margin floor remains intact: "The fact that margins were flat this prior year, given the low volatility... shows you that those marginal retailers are still requiring those higher margins to break even" .

Merchandise Contribution Steady

Merchandise contribution grew 2.1% to $213.2 million on unit margins of 19.6% . Non-nicotine contribution (+4.6%) outpaced nicotine (-1.5%), continuing the category mix shift .

On the nicotine category, management noted Q4 weakness was "really the timing of promotional dollars" but emphasized Murphy USA continues to take share: "We did grow share of market in the cigarette category for both the 4-week and 13-week periods ending January 4th... the business has already normalized in January" . Pouches and other nicotine products continue to show strength .

New Store Momentum

Murphy USA exceeded its 50-store target for 2025, opening 51 new stores during the year and ending Q4 with 1,800 locations . The company put 29 stores into service in Q4 alone .

West highlighted the pipeline strength: "With 2 stores open year-to-date and 18 stores under construction, we are well positioned for sustainable organic growth in the years ahead" .

How Did the Stock React?

Murphy USA shares rose +2.3% on earnings day, closing at $444.85 versus the prior close of $434.84. The stock touched an intraday high of $457.58 (+5.2%) before settling back.

The modest positive reaction reflects solid execution offset by conservative 2026 guidance.

What Did Management Guide?

2026 guidance implies a step-down in profitability, with management projecting net income of $439 million for modeling purposes — approximately 7% below 2025's $470.6 million .

Management noted the guidance assumes 30.5 cpg all-in fuel margins — below Q4's 34.3 cpg run rate . Key assumptions include:

- Volume pressure: Per-store fuel volume expected to decline 1-3% on a same-store basis due to "shifting consumer preferences in a low-price environment"

- OpEx inflation: Store operating expenses per site expected to rise modestly as the company builds larger stores and invests in employees

- SG&A increase: 3-7% growth reflecting investments in technology and people

What Changed From Last Quarter?

Q4 benefited from seasonal margin expansion and accelerated store openings as Murphy USA pushed to exceed its annual target. The company also completed 3 raze-and-rebuild projects in Q4, bringing the full-year total to 23 .

Capital Allocation Update

Murphy USA continues to prioritize aggressive share repurchases alongside organic growth:

The company has $291.9 million remaining under its $1.5 billion 2023 repurchase authorization, with a new $2.0 billion authorization effective upon completion (expires December 2030) .

The dividend was raised 18.9% in September 2025 to $0.63/quarter ($2.52 annualized) .

Balance Sheet & Liquidity

Debt increased $331 million year-over-year to fund share repurchases, with the company drawing $183 million on its $750 million revolver .

Key Risks & Concerns

-

2026 guidance implies earnings decline: Net income guidance of $439M is 7% below 2025's $470.6M, reflecting normalized fuel margins and cost inflation

-

Same-store volume pressure: Management expects per-store fuel volumes to decline 1-3% in 2026 as consumers shift behavior

-

Leverage increasing: Long-term debt rose to $2.2 billion to fund buybacks, though revolver capacity remains ample

-

Nicotine category headwinds: Nicotine contribution declined 1.5% in Q4, continuing a multi-quarter trend

Forward Catalysts

- Q1 2026 earnings (expected May 2026) — Early read on 2026 volume trends and margin realization

- 2026 store openings — First new stores expected in pipeline with 18 under construction

- Fuel margin volatility — Potential upside if market volatility exceeds management's 30.5 cpg assumption

- Potential acquisitions — Management noted guidance range allows for "small bolt-on acquisitions in target markets"

Q&A Highlights

The earnings call Q&A revealed several key insights from management:

Competitive Dynamics

Analyst Bobby Griffin (Raymond James) asked about competitive pressure trends. CEO Mindy West explained the market-by-market dynamics:

"In 2025, some of our stores had average per-store-month volumes that were actually higher. We saw that in 9 states that we operate in. Margins were higher in 10 states... Texas had both higher margins, higher volumes. Colorado and Florida, though, had lower volumes and lower margins."

On competitive entrants: "When a new entrant enters a market, they do exactly what we do. They price very low at the outset while they try to gain their share... that could take three months, six months, a year."

Path to $1.2 Billion EBITDA

Analyst Bonnie Herzog (Goldman Sachs) pressed on the long-term EBITDA target. West outlined three key levers:

- Normalized fuel environment — "The 1.2 does depend on a little more volatility"

- Sustaining 50+ NTIs annually — Each 50-store class generates $35-40M EBITDA at maturity after a 3-year ramp

- Executing on initiatives — "Making our business better is also a material driver"

"As we enter 2027, we will have the 32 new stores from our 2024 build class, the 51 stores from our 2025 build class, and the 45-55 from this year helping to grow EBITDA... That's why we say looking back, 2026 will be viewed as an inflection point."

Operating Expense Management

Analyst Ed Kelly (Wells Fargo) asked about the strong 3.3% OpEx growth in 2025. Management credited several initiatives:

Expected run rate going forward: ~4% per-store expense growth .

Tuck-In Acquisitions

Management discussed the Colorado acquisition strategy: "We got to cherry-pick... It was a market in which we wanted to add density. We were able to get those stores open in less than 30 days."

The company is actively looking at "smaller 1Z, 2Z, 5Z-type acquisitions" .

SNAP Changes Impact

West quantified the SNAP policy changes effective January 1:

- Impact: Less than $5 million headwind

- Exposure: Less than 2% of sales

- Top EBT item: Red Bull

- Affected categories: Candy, Pac-Bev, energy drinks in 5 states

QuickChek Update

The QuickChek brand continues to face pressure. West outlined the turnaround focus:

"We are refocusing on the fundamentals... focusing on the core, which are mainly coffee, breakfast, and sandwich as our traffic drivers. We are simplifying the menu, rationalizing the assortment based on performance, not legacy."

New leadership is in place, with emphasis on "execution and ability to scale are as important as idea generation" .

CEO Transition & Culture Shift

This was CEO Mindy West's first earnings call since taking over. She emphasized cultural evolution:

"We're pushing for things like quicker collaboration, more nimble decision-making, reorganize the company to create more clear roles and accountability. We've already made some leadership changes to help us work better together, remove some inefficient reporting structures."

On strategic priorities: "We need to figure out how to attract and retain new customers, how to grow trips and spend, and how to make our store team's life easier... We're looking at innovation around three main pillars: our portfolio, our customer, and advanced technology."

January 2026 Update

Management noted January is "shaping up to be a good month" while lapping winter storms from 2025 . However, ongoing winter storms in February (impacting the Carolinas) tempered any guidance increase:

"That was one of the reasons, quite frankly, that we were not willing to increase EBITDA guidance materially because we don't know what's gonna happen for the rest of the year."